The New Space Race Will Be Won With Aeroelectric First Stages

Summary:

The first to achieve launch costs of ~$100/kg wins data centers, AI, the internet, global high speed transport, and space. This is the tipping point where data centers move to space to take advantage of much lower cost solar energy and scale exponentially. Scaling rates are so fast that the first to get there will gain a cost reduction advantage that will result in a near unassailable monopoly. Aeroelectric first stages, which can carry the rocket vehicle to high altitude in a fast, safe, and highly reliable manner avoids aero-losses and enables much smaller rocket vehicles. Aeroelectric first stages also enable under half the propellant use, halving launch costs. Small rocket vehicles enable much faster development times and ~100x higher launch rates at a given market size, resulting in a cost reduction curve advantage equivalent to a multiple year lead. With aeroelectric first stages, cost reduction predominantly scales with flight rate, not payload size. This enables aeroelectric first stage launch systems to catch up and overtake large rocket-only reusable launch vehicles in the race to low launch costs. This can happen for ~100x lower costs. Barriers to entry are dramatically lowered, almost anyone with a few million dollars can now achieve low launch costs, enabling an open and competitive launch industry. We are seeking low royalty open licensing of this new technology, and associated advisory roles, in order to scale low-cost launch and space data centers rapidly and win the future of AI.

Aeroelectric first stages:

An aeroelectric first stage is effectively a very large high power and fast multicopter that carries the rocket vehicle to ~20km altitude, above most of the atmosphere, where it can then launch into space. For example, using the 450Wh/kg Amprius lithium battery an aeroelectric first stage to 20km altitude at high subsonic velocities with greater than 50% payload fractions is possible (~6 minutes at maximum discharge rate, which limits speed for this battery). The aeroelectric first stage can return to the launch site and be reflown within an hour at very low costs and much higher reliability than a rocket first stage. As batteries improve performance will increase, enabling supersonic speeds. With a two stage aeroelectric approach higher altitudes and supersonic speeds are possible now, although the additional complexity may or may not be worth it. An aeroelectric multiple flyback booster approach would similarly work and would enable more staging and even larger rocket vehicles. Travelling within the atmosphere generally favors aeroelectric propulsion while travelling above it generally favors rocket vehicles, so the upper atmosphere is a natural staging point, allowing each stage to be optimized for its environment. Aeroelectric stages can scale into the tens of metric tons and very high power electric motors are becoming available, for example, 42kW/kg at 550kW. Using cryogenic cooling via the rocket propellant tanks would enable even larger motors with over 100kW/kg of power - copper has ~5x the electrical conductivity at cryogenic temperatures.

Aeroelectric first stages have numerous advantages over rocket first stages:

All rocket engines can use more efficient vacuum expansion high ISP nozzles as they do not have to operate at sea level.

Gravity losses are largely mitigated so the rocket vehicle can be small and it can fly slowly through the atmosphere, avoiding high aerodynamic loads. This also allows for larger volume payloads.

Launch can occur from little more than a large helicopter pad almost anywhere. Ground takeoff is relatively quiet and safe and launch range costs are largely avoided.

Rocket ignition occurs at altitude, likely over unpopulated areas including out over the sea. The abort options are much better.

With small size the square cube relationship significantly reduces reentry temperatures enabling much easier and longer lived reusable reentry shielding.

Using six axis drone principles, high precision midair capture of the rocket vehicle is possible after reentry, avoiding the need for landing rockets and landing gear, greatly simplifying the rocket vehicle, increasing performance and reducing cost.

In some scenarios the aeroelectric first stage can be used to directly and quickly pick up and transport the rocket vehicle, avoiding the need for launch towers and ground handling.

A significant disadvantage of the aeroelectric first stage is that the staging point is at much lower delta v, shifting much more of the performance burden onto the rocket vehicle. Even so the reusable rocket vehicle might optimally be a single stage, although two stage rocket vehicles also work. Higher rocket engine vacuum ISP, easier reentry, and the elimination of landing systems helps compensate for the higher performance requirement and enables much simpler, safer, lower cost, and faster to develop rocket vehicles with easier design constraints. Testing is much faster and safer, and all stages can return directly to the launch site at high efficiency, enabling rapid turnaround times and very high flight rates and low costs. The prototyping and testing cycle time can be much faster, enabling much faster iteration and learning curves.

Economics:

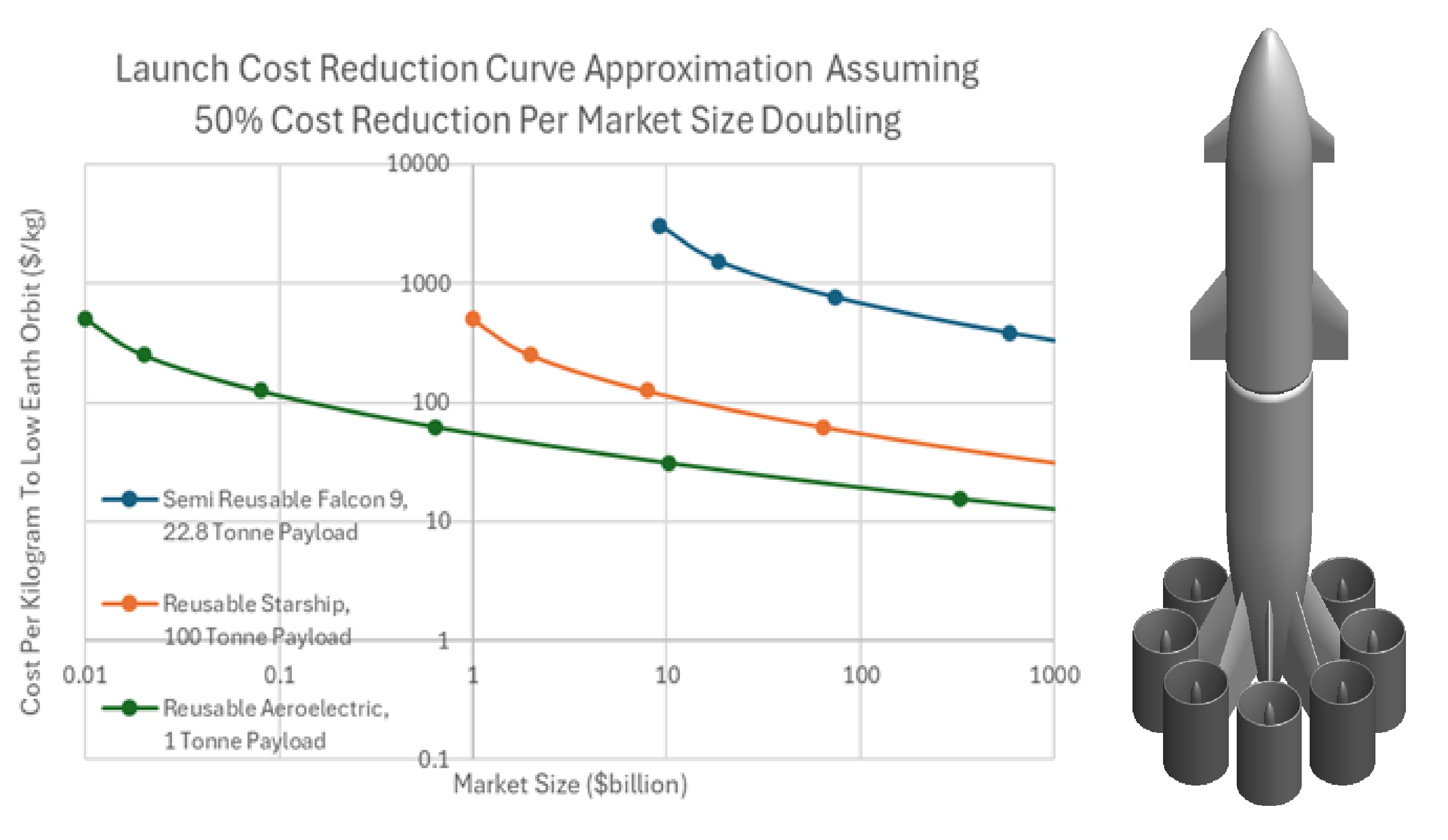

With a two stage rocket vehicle it requires around 10kg of liquified methane to put 1kg of payload in orbit. The index price of natural gas is a little under $0.20/kg so the intrinsic fuel cost is around $2/kg of payload. The cost of mature transport modes is typically around 3x to 5x the fuel or energy cost and launch vehicles would likely cost similarly once they achieve a mature industry status with many hundreds of daily launches (~$10/kg to LEO). With aeroelectric first stages propellant use and total cost can be roughly halved (~$5/kg to LEO), and so aeroelectric first stage launch vehicles can be expected to disrupt two stage rocket vehicles as soon as they reach market scale. Scaling rates and associated cost reduction curves are now dominating technology adoption and markets with continual disruption being the expectation. New technologies can no longer assume a long period of market dominance over which they can generate substantial revenue. Disruption now often occurs even before market maturity is achieved. New technologies need to be optimized around iteration rates, mass production, and scaling rates, if they are to be successful, and aeroelectric first stages enable this.

The current launch industry is predicated on large payloads and very low flight rates. There were only 251 successful launches in 2024 and the total payload launched was around 1,900 metric tons for an average payload size of around 7.5 metric tons. A single aeroelectric first stage would be capable of around 10,000 launches per year and hundreds of aeroelectric first stages would be needed for manufacturing scale. They would need to be distributed around the world for a truly mature and competitive industry. Noting that it takes roughly 90 minutes to orbit the Earth, a fully utilized reusable orbital rocket vehicle, operated in a manner similar to passenger jets, might also achieve up to around 5,000 launches per year. Cost reduction, especially with aeroelectric first stages, scales mostly with flight rate, not payload size, and current markets, even assuming extreme market scaling rates, can not yet support high flight rates. This problem becomes even worse if we assume very large two stage rocket vehicles with ~100 metric ton payloads - only nineteen launches would nominally be needed to serve the entire 2024 market. The need for large launch vehicle sizes is driven primarily by aerolosses that more greatly impact smaller rocket vehicles (largely avoided with aeroelectric first stages), and a lack of orbital assembly capability. Although it may not seem like it, the space launch industry is an immature boutique industry with launch vehicles and payloads largely custom designed and manufactured. There is no shipping container approach to space logistics with the ability to assemble large satellites in space, everything must currently be shipped to space fully assembled (ISS excepted, but it only amplifies this argument).

What the optimal payload size is for a launch vehicle that uses an aeroelectric first stage is not entirely obvious. Smaller payloads enable higher flight rates and lower per mass launch costs for a given market size. There are also some small scale impediments around fixed costs, minimum gauge constraints, low Reynold’s number inefficiencies, and so forth. Human beings are not easily subdivided and should probably use a buddy system for safety. Combined with associated life support and other systems this perhaps suggests a minimum payload capacity of around one metric ton. Satellites would also need to conform to this payload size, which is mostly possible. For context, Starlink satellites weigh around 800kg and Gen 3 Starlink satellites might weigh around two metric tons. Orbital assembly is needed for larger satellites and space missions. In some cases this might be accomplished directly and autonomously in orbit with modular design and docking maneuvers. The availability of much lower cost space launch at smaller payload sizes will favor the development of payloads to match, larger payload sizes will cost more to launch on a per mass basis. With aeroelectric first stages, payloads are also less aerodynamically constrained, they can have proportionately much greater volumes. Interestingly, there are effective ways to construct very large habitat modules and orbital assembly hangars within the one metric ton payload container limit that can then facilitate large scale orbital assembly systems. There are also ways to combine smaller rocket vehicles and aeroelectric first stages to launch much larger payloads while maintaining relatively low launch costs.

To first approximation, a 1 metric ton payload system can achieve the same flight rate and cost reduction as a 100 metric ton payload system at 1/100th the development cost and market scale. Aeroelectric first stages enable this, and while there are still some disadvantages associated with such small scales the same can also be said of much larger launch vehicle scales. At the 1 metric ton payload size an orbital rocket vehicle might have a dry weight as low as 1 metric ton and weigh around 20 metric ton fully fueled with payload. Aeroelectric first stages enable the complete re-envisaging of rocket vehicles and much higher payload fractions. The aeroelectric first stage might also weigh around 20 metric tons. Many different 1 metric ton payload launch systems using an aeroelectric first stage can likely be developed and achieve high launch rates and tipping point launch costs of around $100/kg within 2-3 years, and this might cost less than $100m per effort. Large fully reusable two stage rocket vehicles systems might be able to get to similar flight rates and cost reductions on this time scale, even though they are already decades and billions of dollars into their development and may have already had initial flight tests. The markets necessary to sustain the much larger launch vehicles and the higher flight rates needed may or may not eventuate on this time scale. This would require a ~100x increase in launch market total payload deliveries over the next 2-3 years. Assuming space based data centers this may actually happen, so this could be an interesting race. Given that the development, convenience, and cost reduction curve advantages of smaller aeroelectric first stage launch systems would not end there it would be expected that the larger two stage reusable rocket launch vehicles would lose the majority of the launch market soon thereafter. Or maybe they would adapt to use much larger aeroelectric first stages. Once the potential of aeroelectric first stages becomes apparent, including the consequences of being left behind in the new AI space race, billions of dollars in funding might become available. This would further accelerate the development of aeroelectric first stage enabled launch vehicles - maybe they will happen in less than two years.

Additional markets:

Aeroelectric first stages enable rocket vehicles to reach anywhere on the planet in around an hour at costs comparable to passenger jets. The propellent requirements and costs are significantly less than for orbit and the index cost of natural gas (methane) is around a third that of jet fuel. Aeroelectric first stages enable much higher safety rates than two stage ground launched rocket vehicles and are more compatible with space ports near population centers. The global civil aviation market is around $1 trillion/year and accessing even a small part of this could substantially help with increasing flight rate and reducing cost. Safety would likely significantly limit the size of this market in the short term as it takes many years to develop and demonstrate high safety rates.

In practice the aeroelectric first stage is likely to look more like a heavy lift drone, or multiple heavy lift drones and side mounted electric flyback boosters, rather than a conventional first stage where the rocket engines have been replaced with electric thrusters. A heavy lift drone approach is more suited to ground handling and fast turn around times and also enables easier staging and abort modes. The rocket engines can be ignited and verified prior to release which improves safety and performance. If there is a failure the rocket vehicle can be returned to a safe landing site, perhaps after the propellant tanks have been emptied. The heavy lift drone might also include additional safety systems such as fire suppressant systems. One of the major advantages of the heavy lift drone approach is that the heavy lift drone can also serve other markets. This enables much higher utilization and lower cost. It also enables faster scaling and associated learning and cost reduction curves. The additional applications for heavy lift drones are potentially quite substantial, for example, high speed low-cost logistics. But this might include high value first markets for transporting large packages that might not be easily transported by road. For example, forestry, prefabricated buildings, stranded mining resources, large scale construction, and so forth.

Military Applications:

The direct military applications for aeroelectric first stages are substantial and world changing. Unfortunately most of them are not defensive in nature and they are sufficiently obvious that not raising awareness of them would likely lead to imbalances and a lack of prepared defenses against them. Firstly, space dominance will likely lead to terrestrial dominance. Secondly, the ability to deliver large “packages” anywhere around the world within an hour at very low cost would bypass a lot of military logistics and remove the security associated with distance. Everyone would effectively become close neighbors, and militarily speaking, the world would become a very small place. Thirdly, using small aeroelectric first stages to greatly increase the range of existing “package” delivery devices is another obvious and more immediate threat. This is almost off the shelf technology that is available to almost everyone. Fourthly, using aeroelectric first stages as high altitude high mass flow rate elevators for low-cost glide bombs with ~200km ranges. This is particularly easy, brutal, and currently expensive to defend against, and it may well already be happening. Fifthly, there are many others.

Technology licensing:

Traditional government funding, venture capital, and even large check technology company funding approaches can not scale fast enough to dominate this technology. There are over 1000 electric aircraft companies and over 10,000 space companies. Even if a single company ends up dominating low-cost aeroelectric first stage launch there is no reasonable expectation in being able to select at the outset which one of 1,000s of possible companies it might be. This suggests that a broad, open, and minimal technology licensing approach is needed, along with technology advising, that actively encourages new entrants and helps to support the industry. For example, a progressive technology licensing model is being considered where non-commercial and commercial applications below say $1million in annual revenue are free, annual revenue in the $1 million to $100 million range might be subject to a 0.5% licensing fee, and annual revenues above this might be subject to a 1% licensing fee. This is a race to scale and associated cost reduction curves, so small players will be at a substantial disadvantage. With very fast scaling rates first movers will also find it relatively easy to establish effective monopolies that may not be entirely beneficial to the larger industry. This is a new space race and it is even more consequential than the first one.